Dear East Texas,

Washington’s health care debate has once again missed the mark. Instead of confronting the real drivers of high costs, Democrats continue to push failed Biden-era policies that rely on funneling billions of taxpayer dollars into subsidies while premiums and out-of-pocket costs keep climbing. This week, I voted against the Democrat discharge petition and extension of the Enhanced Premium Tax Credits—a COVID-era program expanded under the Inflation Reduction Act—because masking high prices with more spending is not reform. It’s avoidance. I addressed this vote directly on the House floor, and I encourage you to watch my full remarks explaining why this approach fails East Texas families. |

That floor speech sets the stage for the deeper discussion that follows in this newsletter. Below, I lay out the full picture—how Obamacare subsidies have fueled higher costs, waste, and fraud, and why insurers have thrived while families struggle. I also explain the market-based reforms I’m fighting for to lower costs at the source. East Texans deserve straight answers, not slogans, and real solutions—not endless bailouts.

Background:

During the COVID pandemic, Democrats passed the American Rescue Plan and the Inflation Reduction Act which eliminated income caps for subsidy eligibility and fully subsidized premiums for individuals making less than 150% of the federal poverty level.

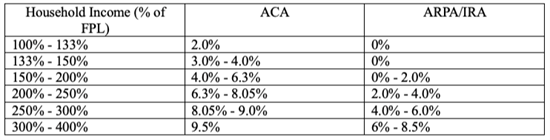

Below is a chart that compares the income amount individuals who are enrolled in ACA plans pay according to their income level.

|

Depending on a household’s income level, they are required to pay that percentage of their income for their plan. For example, if the cost of an ACA plan for a single individual is $6,000 and the individual’s income is $23,5000 that individual would be expected to pay $940. The total tax credit received by that individual would be $5,060.

It’s important to note that only about 7 percent of Americans are enrolled in ACA individual market plans. |

Part I: The Costly Reality of the ACA: Who is Really Paying? |

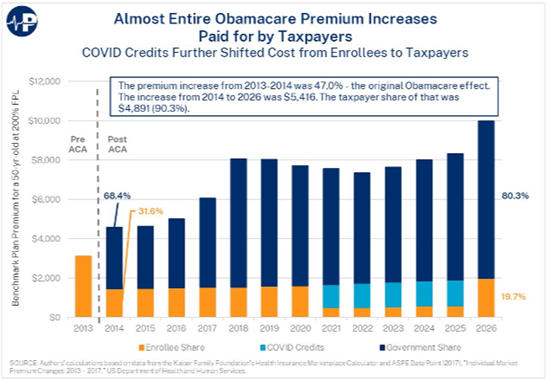

The ACA’s structure guarantees that you, the taxpayer, foot the bill for rising premiums and rampant fraud. 1. Taxpayers Are Paying 90% of the Premium IncreasesWhen the ACA was first implemented, the benchmark plan premium for a typical 50-year-old saw a massive 47.0% increase from 2013 to 2014.

Since then, premiums have continued to climb, and our sources confirm that the overwhelming majority of that cost is shifted onto the federal budget: - The total premium increase from 2014 to 2026 was $5,416.

- Of that increase, the taxpayer share was $4,891, or 90.3%.

|

2. The COVID Credits Fueled Massive Fraud and Waste

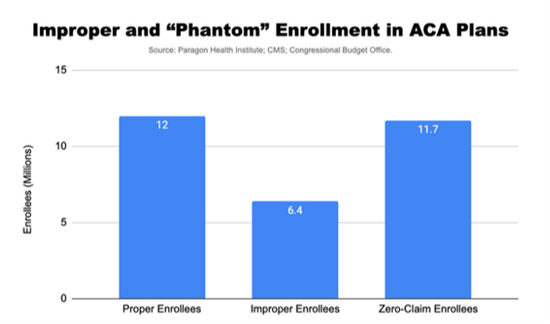

The enhanced subsidies, or "COVID credits," were supposed to be temporary pandemic relief, but they remain—costing at least $40 billion annually. These credits made plans fully subsidized (costing the enrollee $0 a month), which encouraged waste and fraud schemes. - Fraud: Experts estimate there are 6.4 million improper enrollees in the exchanges in 2025, costing taxpayers $27 billion this year alone. The Congressional Budget Office (CBO) estimated that 2.3 million people received credits for which they were not eligible in 2025.

Phantom Enrollment: The lack of any patient contribution ("skin in the game") leads to millions of "phantom" enrollees—people who are covered but never use their plan. In 2024, nearly 12 million enrollees (35% of all exchange enrollees) filed zero claims (no doctor visit, no lab test, no prescriptions) which was an increase of more than threefold in three years following the implementation of the Biden enhanced premium tax credits. For the free, fully-subsidized plans, 40% had zero claims. The number of zero-claims enrollees in private plans is generally around 15 percent which is significantly less than those in ACA plans.

|

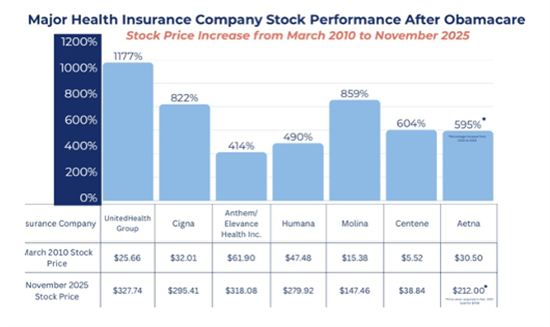

The simple truth is that the policy results in sending money directly to health insurance companies. Since the ACA became law, major insurer stock prices have soared; for example, UnitedHealth Group saw an increase of 1,177%. |

GAO Investigation:

Recently, the Government Accountability Office (GAO) released a report that shows the Affordable Care Act’s exchange is vulnerable to fraud. Specifically, this report revealed that 23 of 24 fictitious applicants were approved for ACA health plans by using fake Social Security numbers, unverifiable identities, and submitting income levels that would have required documentations but was never presented. 100% of the fake applicants were approved for ACA plans. For 2025, 18 of the fictitious enrollees were still enrolled in Obamacare. This type of fraud is appalling yet Democrats opposed commonsense fraud protections that were included in the Working Families Tax Cut. |

Part II: Our Solutions—Building on What We’ve Already Done |

House Republicans, including myself, have been fighting for real alternatives that introduce competition and cut costs at the source. A. Accomplishments: Restoring Integrity in the WFTCAWe recently passed the Working Families Tax Cut Act (WFTCA) to enact crucial "America First" reforms aimed at strengthening the health system for citizens and addressing fraud.- Ending Taxpayer Funding for Illegal Immigrant Healthcare: The WFTCA prohibits the federal government from subsidizing healthcare—including Medicaid, Medicare, and ACA subsidies—for non-citizens who do not meet strict eligibility requirements. This reform saves over $165 billion over the next decade by tightening ACA and Medicaid rules and closing loopholes.

- Fighting Fraud and Waste: The WFTCA restored basic program integrity measures by ensuring that exchanges must confirm eligibility (including immigration status) prior to any individual receiving an ACA premium subsidy. Crucially, it ended the automatic re-enrollment of unverified people into subsidized plans, saving an estimated $41.3 billion.

B. The Path Forward: Cutting Costs and Empowering YouTo truly lower costs and end the expensive, fraud-ridden subsidy cycle, we must pass the following key measures:

1. Lowering Premiums by Funding Cost-Sharing Reductions (CSRs): We previously passed a provision in the House that would have funded CSR payments. This is a common-sense reform that directly reduces patient out-of-pocket costs and was estimated to lower ACA premiums by over 10 percent, saving $30.8 billion over 10 years. This is a proven way to make insurance cheaper immediately.

2. Attacking Hidden Drug Costs through PBM Reform: We must address the real driver of skyrocketing health care costs: the middleman monopolies. We need reforms to rein in Pharmacy Benefit Managers (PBMs), which act as middlemen and take kickbacks, driving up prescription drug prices for consumers. Our proposals would: - Require PBMs to use transparent pricing models in Medicaid based on a drug’s ingredient cost plus a professional dispensing fee.

- Prohibit PBMs in Medicare from receiving compensation related to dispensing drugs other than legitimate service fees.

3. Empowering East Texas Families and Small Businesses (Our Solutions): We believe in creating competition, not subsidizing insurance companies. Our focus is on empowering individuals and employers with account-based, affordable options: - Expanding Health Savings Accounts (HSAs): We must expand HSA eligibility to allow individuals to contribute to an HSA while participating in direct primary care arrangements. We also allow those in lower-cost bronze-level or catastrophic plans on the exchange to make HSA contributions. This overall package was projected by the CBO to reduce premiums.

- CHOICE for Small Business: We must codify Individual Coverage Health Reimbursement Arrangements (ICHRAs), or CHOICE arrangements. This would give small businesses (fewer than 50 employees) a two-year tax credit to help them offer employees new, flexible health coverage options. This puts power back in the hands of employers and employees.

|

Conclusion: Real Solutions for Real Costs |

The ACA, the "(Un)Affordable Care Act," has fundamentally failed East Texas taxpayers by prioritizing massive subsidies that mask surging premiums and finance widespread fraud. This reliance on temporary government giveaways and the lifting of the income cap resulted in $27 billion in improper spending in 2025 alone and allowed millions of phantom enrollments that only benefit big insurance companies.

We must reject the approach of subsidizing insurance companies and instead choose to create competition. Our policy solutions are grounded in structural reform that tackles the real issue: the high cost of care. By aggressively pursuing market-based mechanisms—from enacting PBM reform to attack high drug prices, to realizing cost-saving measures like funding CSRs, and empowering individuals through HSAs and expanding CHOICE Arrangements—we put the patient and the taxpayer back in control.

Allowing the temporary, fraud-ridden COVID credits to expire restores financial integrity and shifts the focus back to these core Republican reforms that will deliver lasting affordability and competition to the health care market. Our commitment is to real, long-term solutions, ensuring that affordable, quality care is achieved through competition, empowerment, and fiscal responsibility, not endless taxpayer bailouts.

This fight is not about cutting coverage; it is about ending fraud and lowering the underlying cost of care for every American family. |

On January 5, 1933 construction began on the Golden Gate Bridge. The bridge was completed in May 1937and opened to pedestrians on May 27, 1937, with over 200,000 people walking, running, and even roller-skating across the span. It opened to vehicular traffic the next day, on May 28, a triumph of engineering that came in under budget at approximately $35 million. The iconic color, "International Orange," was chosen by architect Irving Morrow to blend with the natural surroundings and provide high visibility. |

Dealing with federal agencies can be complicated, and my office is here to help. If you need help with Social Security, the IRS, passport renewals, the VA, or other federal agencies, please do not hesitate to reach out to my office by calling (903) 561-6349 or visiting my website.

It is an honor to be your voice in Congress.

With gratitude, |

Nathaniel Moran Member of Congress |

Answer to Last Week's Texas Trivia Question

⬇️ What major U.S. highway, also known as the "Main Street of America," runs through Texas from north to south? |

|

This Week's Texas Trivia Question Which founding member of the legendary band The Eagles, known for hits like "Hotel California," hails from East Texas? Check back next week for the answer! |

|

|